Fuel Cost Calculator

Budget for your daily commute or your next road trip.

Get quotes from providers in your area

Last updated: June 5, 2026

Enter trip details, your car’s fuel efficiency (mpg), and the cost of gas to see how much you can expect to pay.

If you’re not sure of your car’s fuel efficiency, you can find estimates by vehicle type below the calculator.

Fuel Cost Calculator

Your Trip Cost Breakdown

$0.00Total fuel cost

0.0 galFuel needed

$0.00Cost per mile

Fuel costs add up, but car insurance doesn't have to. Lower your monthly costs today.Get My Free Quote

Fuel costs add up, but car insurance doesn't have to. Lower your monthly costs today.Get My Free Quote* Total Fuel Cost, Fuel needed, and Cost per mile shown are estimates based on the data provided above. Actual cost and fuel may vary on additional factors.

Fuel Efficiency Estimates by Vehicle Type

| Vehicle type | Approximate mpg |

|---|---|

| Sedan | 32 |

| Small SUV | 30 |

| Mid-size SUV | 25 |

| Large SUV | 20 |

| Pickup truck | 21 |

| Small hybrid | 50 |

| Large hybrid | 36 |

| Minivan | 24 |

How Our Fuel Cost Calculator Works

One-Time Trip

Let’s say you’re driving 500 miles round trip in your 2019 Honda Civic, which gets an average of 36 miles per gallon. Our calculator divides the total number of trip miles (500) by your car’s mpg (36) to find the number of gallons you’ll use during the trip — in this example, about 14 gallons.

Next, let’s say where you live, the average cost of a gallon of gas is $4.10. The calculator multiplies the number of gallons you’ll use by the cost of fuel, and the result is the cost for your trip: $57.

| Total number of miles driven | 500 |

| Vehicle average mpg | 36 |

| Gallons of gas used during trip (total miles ÷ mpg) | 14 |

| Average cost of gas per gallon | $4.10 |

| Total trip cost (gallons used x cost per gallon) | $57 |

3- or 5-day-per-week trip

Follow a similar process to determine the cost of fuel for your daily commute. Let’s say you commute five days a week and live 20 miles from work; enter 40 miles (the daily round trip total) into the calculator.

Our calculator divides your daily mileage by your vehicle’s mpg. If you drive a 2019 Honda Civic which gets 36 mpg, you’ll use about 1.11 gallons of gas daily.

Finally, it multiplies the gas you use by the cost of fuel. Let’s say the cost of gas where you live is $4.10 per gallon. That means you’ll spend around $4.55 daily on your commute. If you drive to work five days a week, fifty weeks a year, that’s about $23 weekly, $90 monthly, or $1,140 annually.

BUDGETING

The average American household spends $150 to $200 on gas every month. Transportation is usually the second-most expensive budget category, after housing.

| Daily commuting mileage | 40 |

| Vehicle average mpg | 36 |

| Gallons of gas used daily (commute ÷ mpg) | 1.11 |

| Average cost of gas per gallon | $4.10 |

| Daily commuting cost (gallons used x cost per gallon) | $4.55 |

| Weekly commuting cost (daily cost x 5 days) | $22.76 |

| Monthly commuting cost (weekly cost x 4 weeks) | $91 |

| Annual commuting cost (weekly cost x 50 weeks, assuming 2 weeks vacation) | $1,138 |

How much gas will $10 or $20 get me?

Based on average gas prices and fuel efficiency, $10 will currently get you about 2.3 gallons of regular unleaded gas and last you around 58 miles; $20 will get you 4.7 gallons and last about 117 miles.

Here’s a breakdown:

| Cost of gas | $4.29/gallon |

|---|---|

| Number of gallons $10 can buy ($10 ÷ $4.29/gal) | 2.3 gallons |

| Number of gallons $20 can buy ($20 ÷ $4.29/gal) | 4.7 gallons |

| Fuel efficiency in miles per gallon | 25 mpg |

| Distance on 2.3 gallons, or $10 worth of gas (25 mpg x 2.3 gallons) | ~58 miles |

| Distance on 4.7 gallons, or $20 worth of gas (25 mpg x 4.7 gallons) | ~117 miles |

The table below gives you an idea of how much gas you can get, assuming 25 MPG fuel efficiency and $4.29 cost per gallon.

| Money Spent | Gallons of Gas | Miles You Can Drive |

|---|---|---|

| $5 | 1.2 | 29 |

| $10 | 2.3 | 58 |

| $15 | 3.5 | 87 |

| $20 | 4.7 | 117 |

| $25 | 5.8 | 145 |

| $30 | 7 | 175 |

| $40 | 9.3 | 233 |

| $50 | 11.6 | 291 |

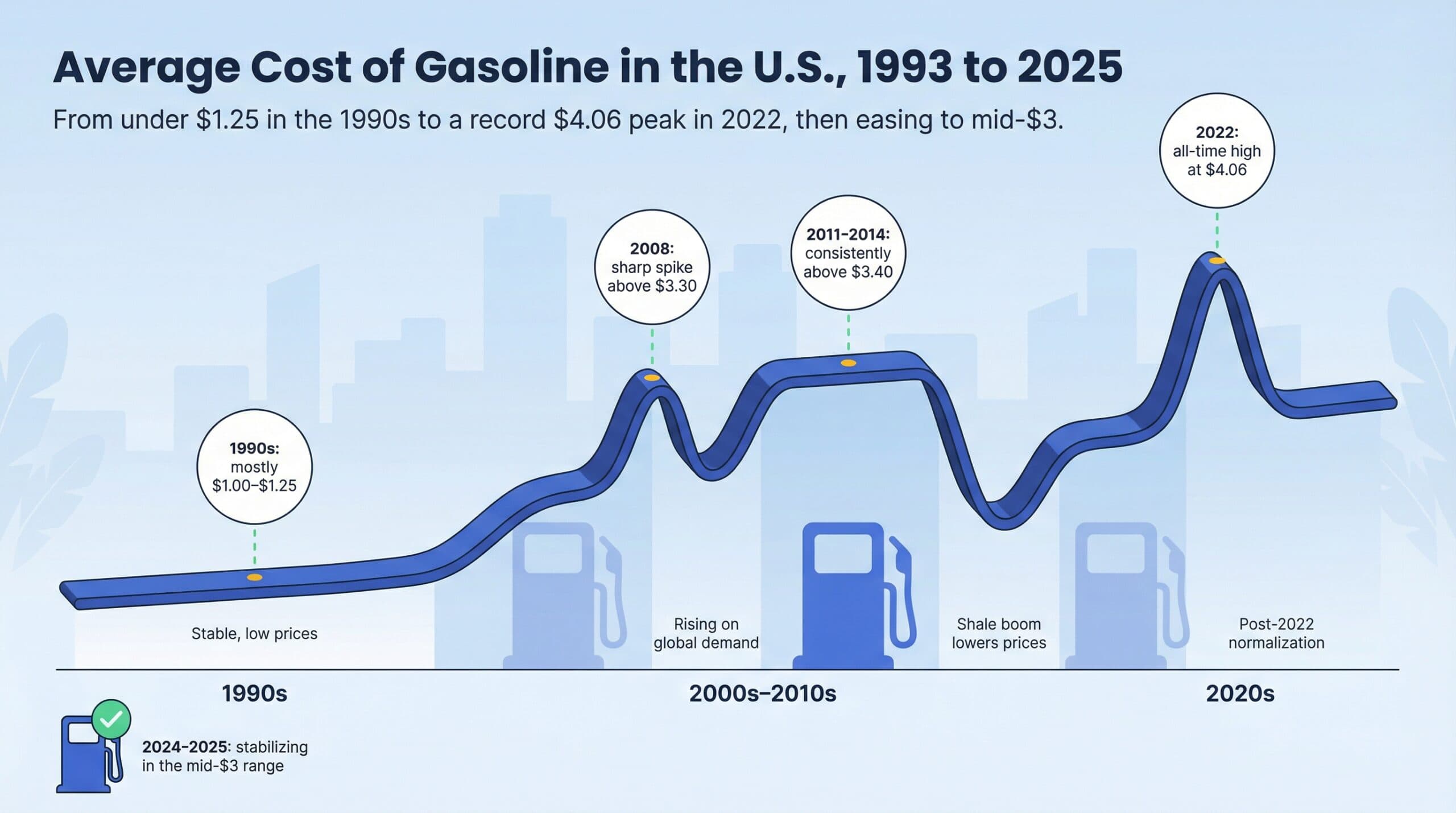

Average Cost of Gasoline in the U.S., 1993 - 2026

U.S. gas prices rose from under $1.25 in the 1990s to a record peak of $4.06 in 2022 before easing to the mid-$3 range.

1990s: Gas prices remained stable and low, hovering around $1.00 to $1.25 per gallon.

2000s: In the early 2000s, prices climbed due to global demand, geopolitical tensions, and supply constraints. They peaked in 2008 at over $3.30, then dropped in 2009 and 2010 during the financial crisis.

2010s: Prices were above $3.40 during 2011–2014 amid tight global oil markets. A major shift occurred in 2015–2016 with the shale oil boom, which increased supply and pushed prices down to the low $2 range. Prices then gradually rose through 2018.

2020s: Gas prices lowered in 2020 due to the pandemic, then spiked post-pandemic—reaching an all-time high of $4.06 in 2022. Prices then stabilized in the mid-$3 range by 2024–2025. This has shifted recently: as of June 2026, gas prices have risen to $4.29 due to supply disruptions and geopolitical conflict.

| Year | Average Annual Price (USD per Gallon)1 |

|---|---|

| 1993 (April through December average) | 1.071 |

| 1994 | 1.086 |

| 1995 | 1.167 |

| 1996 | 1.236 |

| 1997 | 1.245 |

| 1998 | 1.072 |

| 1999 | 1.175 |

| 2000 | 1.525 |

| 2001 | 1.466 |

| 2002 | 1.385 |

| 2003 | 1.601 |

| 2004 | 1.970 |

| 2005 | 2.314 |

| 2006 | 2.615 |

| 2007 | 2.846 |

| 2008 | 3.305 |

| 2009 | 2.488 |

| 2010 | 2.834 |

| 2011 | 3.576 |

| 2012 | 3.686 |

| 2013 | 3.570 |

| 2014 | 3.442 |

| 2015 | 2.513 |

| 2016 | 2.257 |

| 2017 | 2.532 |

| 2018 | 2.827 |

| 2019 | 2.682 |

| 2020 | 2.260 |

| 2021 | 3.094 |

| 2022 | 4.064 |

| 2023 | 3.676 |

| 2024 | 3.400 |

| 2025 | 3.226 |

| 2026 (as of June) | 4.290 |

How much gas is used per mile?

It depends on the car, but on average about 0.04 gallons of gas is used per mile, or one-twenty fifth of a gallon. The exact number of gallons used per mile depends on your car’s fuel efficiency. The average MPG for a car in the US is around 25, which equates to 0.04 gallons per mile.

| Vehicle Fuel Efficiency (MPG) | Gallons of Gas Used per Mile | Common Vehicle Type |

|---|---|---|

| 10 | 0.1 | Heavy-duty truck / Large SUV (towing) |

| 15 | 0.067 | Large pickup truck / Large SUV |

| 20 | 0.05 | Mid-size SUV / Pickup |

| 25 | 0.04 | Small SUV / Minivan |

| 30 | 0.033 | Compact car |

| 35 | 0.029 | Efficient compact / Small hybrid SUV |

| 40 | 0.025 | Small hybrid car |

| 45 | 0.022 | Very efficient hybrid |

| 50 | 0.02 | High-efficiency hybrid |

Simple Ways to Save on Gas

This infographic visualizes simple and effective methods for drivers to reduce their fuel consumption and save money.

Change Your Driving Habits for Immediate Savings

Lower gas mileage equates to higher fuel costs. Aggressive driving—like rapid acceleration, speeding, and hard braking—can lower your gas mileage by as much as 15 to 30 percent at highway speeds, and 10 to 40 percent in stop-and-go traffic.2 To maximize your savings:

- Accelerate and brake gently.

- Maintain a steady speed whenever possible; use cruise control on highways.

- Avoid excessive idling—it can use up to half a gallon of gas per hour.

- Remove unnecessary weight from your vehicle (like unused roof racks or cargo).

Did You Know?

If you spend $2,000 a year on gas, simply adopting smoother driving habits could save you up to $600 annually—without any special equipment or major lifestyle change.

Carpool

Sharing a ride — for example, driving to work with a colleague or offering to split driving duties with other parents — is a great way to reduce spending on fuel (as well as reduce wear and tear on your vehicle). Carpooling, taking public transportation, walking, or biking just one day a week can save the typical commuter up to 1,200 miles every year, or an average of $455.3

Choose another form of transportation

Gas prices are a major concern for most Americans. According to J.D. Power, the typical household spends $2,449 on fuel annually, or a little over $200 monthly.4 Additionally, the cost of vehicles themselves has risen sharply since the COVID-19 pandemic began. Biking, walking, and taking public transportation are often far less expensive than driving — and less stressful. Experiment with taking an alternate form of transportation to work, even just one day a week, to save time and money on gas.

Check your tire pressure

Properly inflated tires can improve your gas mileage by up to 3 percent and will last longer, saving you money on maintenance.5 Check your tire pressure every month or so, using the sticker inside your driver door (or your vehicle manual) to see the proper pressure. It’s best to adjust tire pressure when your tires are cold, before you’ve driven. You can buy a digital air compressor for about $30.

Keep up on vehicle maintenance

A well-maintained engine operates more efficiently, leading to better gas mileage. Regularly change your oil and replace air filters. Using the manufacturer’s recommended grade of oil and opting for “energy conserving” oil can contribute to fuel savings. Energy-conserving oils contain additives that reduce friction, making the engine more efficient and improving gas mileage.

TIP:

Search the U.S. Department of Energy’s website to find your car’s mpg at https://www.fueleconomy.gov/feg/findacar.shtml.

Drive the speed limit

Speeding is worse for your fuel economy (not to mention, a speeding ticket will increase the cost of auto insurance). Avoid aggressive driving, such as rapid acceleration and hard braking, as it consumes more fuel. Maintain a steady speed and use cruise control on highways to optimize efficiency.

Plan efficient trips

The less you drive, the less you’ll spend on fuel. Try to consolidate errands into a single trip, rather than multiple separate trips. In a city, if possible park in a central location and walk to your different appointments, as stop-and-go traffic is worse for gas mileage.

DID YOU KNOW?

Research has found that driving is the most stressful method of commuting.6

Consider a more fuel-efficient vehicle

When you’re in the market for another vehicle, it’s worth comparing hybrid, electric, and gas-powered options—not just by MPG, but by long-term savings in fuel and ownership costs.

Hybrids get about 40 percent more miles per gallon than traditional gas-powered cars, meaning you’ll fill your tank less often and save hundreds of dollars annually.7 For instance, upgrading from a 25mpg gas car to a 50mpg hybrid, driving 12,000 miles/year at $4.25/gallon, could save you over $1,000 on fuel alone per year.

Electric cars often cost even less to “fuel” per mile and can have lower maintenance costs, though they may cost more to purchase and require access to home or public charging.

Here are some of the most fuel-efficient hybrid cars:

| Vehicle | Combined mpg | Estimated annual fuel cost savings* |

|---|---|---|

| 2025 Toyota Prius LE | 57 | $1,145 |

| 2024 Toyota Corolla | 53 | $1,078 |

| 2025 Kia Niro LX | 53 | $1,078 |

| 2024 Toyota Camry LE | 52 | $1,059 |

| 2019 Toyota Prius | 52 | $1,059 |

| 2023 Hyundai Elantra | 52 | $1,059 |

| 2015 Toyota Camry Hybrid | 41 | $796 |

| 2011 Mercury Milan Hybrid | 41 | $796 |

| 2010 Ford Fusion Hybrid | 41 | $796 |

| 2014 Toyota Avalon Hybrid | 40 | $765 |

Here are some of the most fuel-efficient gas-powered (non-hybrid) cars:

| Car Model | Combined mpg | Estimated annual fuel cost savings* |

|---|---|---|

| 2024 Mitsubishi Mirage | 39 | $732 |

| 2023 Hyundai Elantra SE | 37 | $662 |

| 2023 Toyota Corolla | 36 | $623 |

| 2020 Honda Fit | 36 | $623 |

| 2015 Honda Civic HF | 35 | $583 |

| 2020 Toyota Yaris | 35 | $583 |

| 2023 Honda Civic | 35 | $583 |

| 2023 Kia Forte LX | 35 | $583 |

| 2017 Nissan Versa | 35 | $583 |

| 2015 Chevrolet Spark | 34 | $540 |

* Estimated annual fuel cost savings are calculated based on upgrading from a 25 mpg car, driving 12,000 miles annually, and assuming a cost of gas at $4.25 per gallon.

>>RELATED: Looking to cut vehicle costs? Check out our guide to the best cheap auto insurance.

Factors that Determine Fuel Price

Cost of Crude Oil

The primary factor influencing gas prices is the cost of crude oil, often accounting for over 50 percent of price.8 Changes in global oil supply and demand, geopolitical events, and decisions by oil-producing nations, especially those in the Organization of the Petroleum Exporting Countries (OPEC), can impact crude oil prices. For example, Russia’s invasion of Ukraine increased the cost of crude oil significantly. Government intervention also plays a role; for example, when former President Joe Biden released oil from U.S. strategic reserves to lower costs.

Taxes

Federal, state, and local taxes contribute to the cost of gas. For example, one of the reasons gas is more expensive in California is that its tax on gasoline is higher than those of other states, accounting for about 13 percent of the price of a gallon of gas.9

Distribution and Marketing Costs

The process of distributing and marketing gasoline involves costs related to transportation, storage, and the operation of gas stations. Distribution costs can vary based on the location and infrastructure.

Market Forces and Speculation

Like other commodities, the price of gas is influenced by market forces and speculation. Factors such as global economic conditions, supply and demand dynamics, and market speculation can contribute to price volatility.

Fuel Cost FAQ

Combine trips, carpool, and keep your tires properly inflated. Avoid aggressive driving and try to drive at steady speeds.

Look inside your driver’s door, check your owner’s manual, or use the search tool at fueleconomy.gov.

Yes—many insurers now offer usage-based or pay-per-mile policies that can lower your premium if you drive less.

Google Maps does not currently estimate fuel cost. However, you can select your engine type and Google Maps will show you the most fuel-efficient route. You can also set the app to automatically use the most fuel-efficient route if the arrival times are similar.

To calculate the amount of gas needed, you can use the following formula:

Total Distance ÷ Miles Per Gallon = Gallons of Gas Needed

For example, if you’ll be driving an average of 60 miles per hour and your car gets 25 miles per gallon, you’ll need about 2.4 gallons of gas for your trip. If the cost of gas is $4.39 per gallon, your hour-long trip will cost $10.50.

| Total Distance | 200 miles |

| Miles per Gallon | 30 |

| Gas needed (Total Distance ÷ Miles Per Gallon) | 6.67 gallons |

The cost of gas to drive for 1 hour depends on several factors, including the fuel efficiency of your vehicle, the current price of gas, and your driving conditions. To estimate the cost, you can use the following formula:

(Average Speed in mph ÷ Miles per Gallon) x Price per Gallon

For example, if you’ll be driving an average of 60 miles per hour and your car gets 25 miles per gallon, you’ll need about 2.4 gallons of gas for your trip. If the cost of gas is $4.29 per gallon, your hour-long trip will cost $10.30.

| Average speed (mph) | 60 |

| Miles per Gallon | 25 |

| Gas used in 1 hour (60 mph ÷ 25 mpg) | 2.4 |

| Cost of gas per gallon | $4.29 |

| Cost of hour-long trip (Gallons x Cost) | $10.30 |

Mileage can increase your insurance, because the more you drive, the higher the chance of getting into an accident. Some insurance companies offer usage-based insurance and pay-per-mile insurance, which lower your premium if you drive fewer miles.

Sources

Petroleum & Other Liquids. U.S. Energy Information Administration. (2025).

https://www.eia.gov/dnav/pet/hist/LeafHandler.ashx?n=PET&s=EMM_EPM0_PTE_NUS_DPG&f=MDriving More Efficiently. Energy Saver (U.S. Department of Energy). (2025).

https://www.energy.gov/energysaver/driving-more-efficientlyAlternative Transportation Facts. City of High Point. (2025).

https://www.highpointnc.gov/664/Alternative-Transportation-FactsHow Much Do People Spend on Gas Each Month?. J.D. Power. (2024, Dec 05).

https://www.jdpower.com/cars/shopping-guides/how-much-do-people-spend-on-gas-each-monthKeeping Your Vehicle in Shape. FuelEconomy.gov. (2025).

https://www.fueleconomy.gov/feg/maintain.jspAm stressed, must travel: The relationship between mode choice and commuting stress. Transportation Research Part F: Traffic Psychology and Behaviour, Science Direct. (2015, Oct).

https://www.sciencedirect.com/science/article/abs/pii/S1369847815001370Why Hybrid Vehicles Are a Smart Choice Right Now. Consumer Reports. (2025, Mar 11).

https://www.consumerreports.org/cars/hybrids-evs/why-hybrid-vehicles-are-a-smart-choice-right-now-a2736240282/Gas Prices Explained. U.S. Oil & Gas Association. (2025).

https://usoga.org/gas-prices-explained/Transportation Frequently Asked Questions. Legislative Analyst’s Office. (2025).

https://lao.ca.gov/Transportation/FAQs

Related Articles

How Inflation Affects the Cost of Car Ownership

September 30, 2024

Virginia Car Insurance Laws and Requirements

May 22, 2026