Does Car Insurance Follow the Car or the Driver? A Guide to Borrowed Car Coverage

Learn how coverage works for a car you borrow or loan.

Get quotes from providers in your area

Last updated: July 28, 2026

If you frequently borrow or loan a vehicle, it’s important to understand how coverage works for that vehicle, especially so you know what to expect if an accident happens. Below, we’ve broken down important details about borrowed car coverage so you can rest assured knowing you’re covered no matter the scenario.

Driving a borrowed ride? Farmers has you covered.

Protect yourself when the car’s not yours but the responsibility is.

Two Things You Need to Know First

Does insurance follow the car or the driver? As a general rule, car insurance follows the car, not the driver. That means the vehicle owner’s policy is typically the first line of coverage in an accident, regardless of who’s behind the wheel, as long as that person had permission to drive.

Can someone else drive my car and still be covered? Yes. Most auto policies include a permissive use clause, which allows the owner to lend their car occasionally to someone else without losing coverage. If you let a friend or family member borrow your car now and then, your policy extends to them for that trip. They must be a licensed, non-excluded driver using the car for personal reasons.

With that in mind, here’s how borrowed car coverage actually works, and where the exceptions kick in.

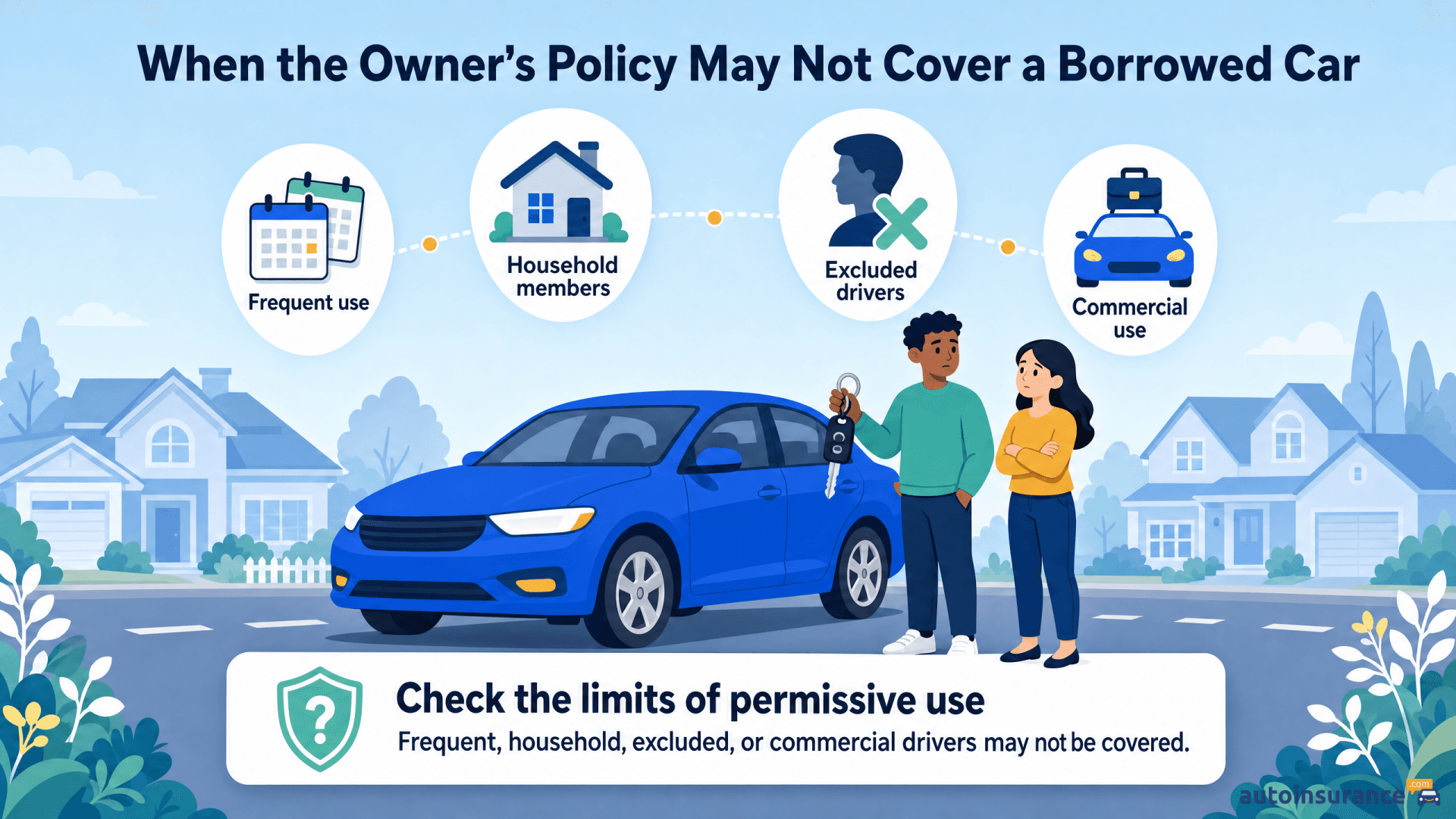

When Does the Owner's Policy Not Cover a Borrowed Car?

Certain scenarios like frequent use or commercial driving can invalidate insurance coverage for borrowed vehicles.

Permissive use has limits. In the following situations, the owner’s policy may not apply, and both the owner and borrower should take extra precautions:

- Frequent borrowers. Permissive use means occasional, casual use. If someone regularly borrows the same car, they should be added to the owner’s policy.

- Household members. Living with the car owner doesn’t automatically mean you’re covered. If a household member drives the car often, most insurers expect that person to be added to the policy.

- Excluded drivers. If a driver has been explicitly excluded from a policy because of a poor driving record, they are not covered under any circumstances. Owners should think carefully before letting an excluded driver take the wheel.

- Commercial use. If the car is being used for business purposes, such as rideshare or delivery driving, a standard personal auto policy isn’t enough. Commercial auto insurance is required.

The same rules apply in reverse: if you’re the one frequently borrowing someone else’s car, these exceptions can leave you without coverage too.

Non-Owner Insurance: An Option for Frequent Borrowers

It may be a good idea to purchase non-owner insurance if you borrow or rent cars frequently and drive them long distances, especially if you can’t get added as a secondary driver on the owner’s policy.

Non-owner insurance covers bodily injury and property damage in the event of an accident, but it doesn’t cover vehicle damage or your own injuries. Generally, rates for non-owner insurance are less expensive than standard auto insurance costs.

Non-owner insurance kicks in if the limits of the owner’s policy are reached, or if you are explicitly excluded from their policy. It can sometimes pay for personal injury or medical expenses, but it depends on the policy.

TIP

Consider purchasing non-owner car insurance if you share or rent cars often, but be aware that it may not cover damage to the vehicle you operate.

Primary vs. Secondary Insurance Coverage

When a borrowed car is in an accident, coverage usually works in a specific order:

- Primary insurance: The car owner’s policy is billed first.

- Secondary insurance: The borrower’s own policy, if they have one, may cover costs the primary policy doesn’t.

For example, if a borrower causes an accident and the owner’s policy doesn’t cover the full cost, the borrower’s own insurance may cover the remaining amount. If the borrower has no insurance, or their policy excludes this situation, the car owner may have to pay the difference out of pocket.

However, none of this applies if you never gave permission to drive your car — like in an auto theft or an explicit refusal. That said, except in cases of theft, proving lack of permission to an insurer can be difficult.

GOOD TO KNOW

If you live in the same household as the car borrower, you may be required to list them on your policy.

Can You Get Car Insurance Without a License?

You don’t legally need a driver’s license to purchase car insurance, though not every insurer will sell you a policy without a license. This situation often comes up for car owners who don’t drive themselves but need coverage for others who use the vehicle.

Providers like The Hartford offer this coverage to unlicensed owners. In these cases, the policy lists the owner as an excluded driver on their own policy, reducing risk for the car insurance company while insuring other drivers who operate the vehicle.

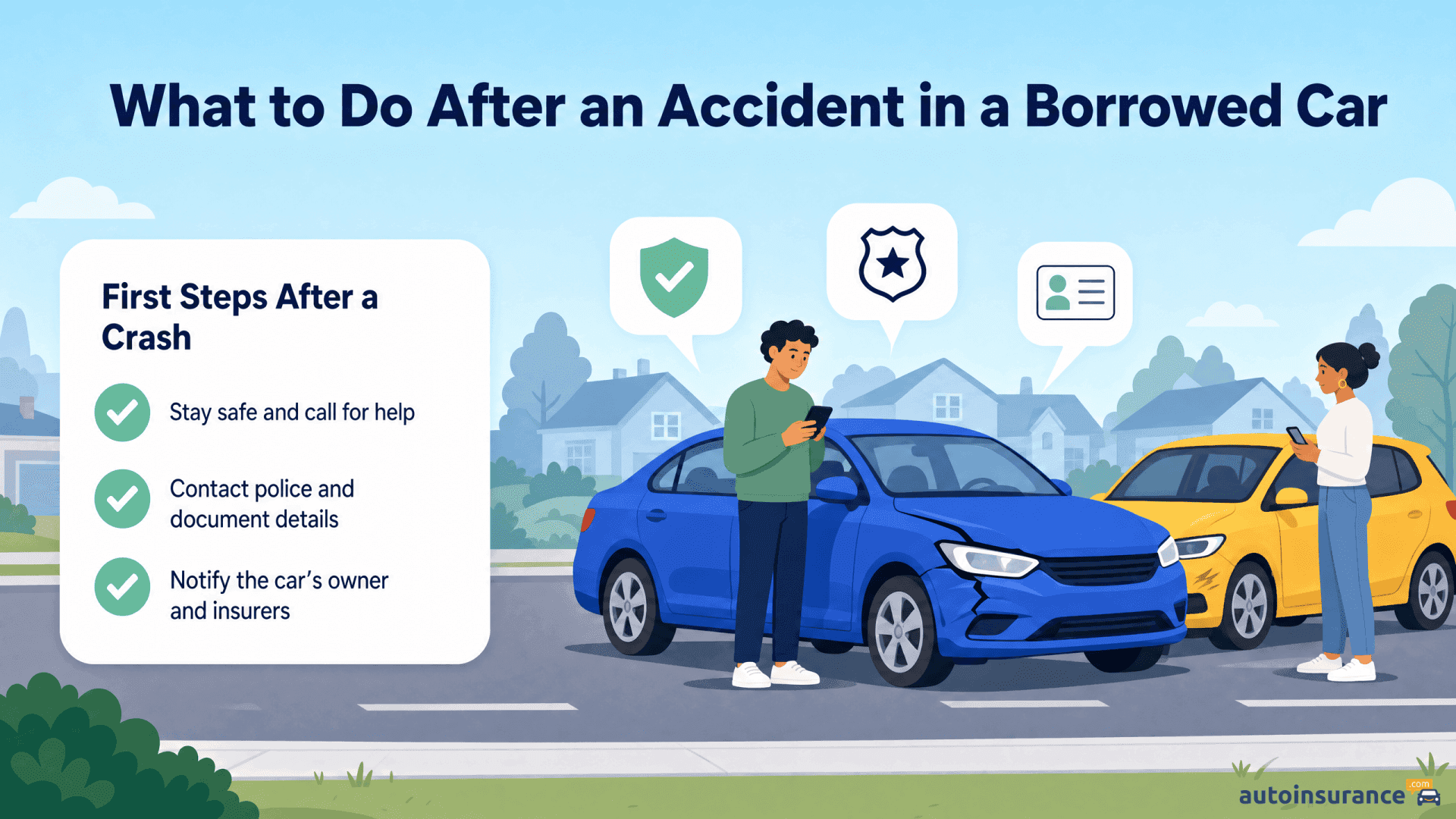

What to Do After Getting Into an Accident in a Borrowed Car

Drivers should prioritize safety, document the scene, and notify the vehicle owner and insurance companies immediately.

All the usual tips apply in the event of an accident if you are driving a borrowed car:

- Remain at the scene. Call an ambulance if there are any injuries.

- Contact the police and file a report. Get the names and badge numbers of all the officers involved. You’ll want to include the police report in your claim. Get a copy of the police report for your files.

- Gather important info. Document the vehicle damages, the vehicle identification numbers of all the cars involved, and the names, contact information, and insurance information of everyone involved. Write down the date, time, and weather conditions of the accident. Take pictures of the damages.

- Contact the person you borrowed the car from. They can file an insurance claim for you, or they might have you file the claim. If their insurance is insufficient and you have insurance, you may have to file a claim with your own provider.

- If the accident wasn’t your fault, file a third-party claim with the at-fault party’s insurance provider for bodily injury or property damage. You can also file a claim with the car owner’s insurer, who can seek reimbursement through subrogation.

- If the accident was your fault, file medical payments and collision claimsto reimburse you for your injuries and damages. If you lack these coverages, you will have to pay out of pocket for your medical costs and property damage, as well as the other party’s.

Before You Borrow or Loan a Car

- Check your policy first. If you don’t understand your policy, contact your insurance agent or broker directly.

- Only lend your car to people you trust. Choose responsible friends and relatives with good driving records to avoid accidents.

- Set clear expectations. This includes how long the car is needed, what it will be used for, and its condition when returned.

- Take photos of the car to ensure that your provider will cover new damages.

Questions to Ask if You’re Loaning or Borrowing a Vehicle

If you’re loaning your car, ask the borrower:

- Are you a capable, confident driver?

- Are you licensed?

- Do you have your own car insurance?

- If so, what coverage does it provide?

- How long do you need the car?

- When do you plan to return the car?

- What do you plan to use the car for?

If you’re borrowing a car, ask the owner:

- Do I have permission to borrow the car?

- Where is the registration and insurance information?

- Do you have car insurance that covers me in an accident?

- Does your car have any issues or quirks I should know about?

The Bottom Line

Borrowing a car is usually straightforward from an insurance standpoint, thanks to permissive use coverage. However, the owner’s policy may not apply in situations that involve frequent use, household members, excluded drivers, and commercial activity. If you’re unsure, contact your insurance agent before you hand over the keys to ensure your vehicle is always covered.

Frequently Asked Questions

Yes, most insurance companies will raise your premiums after an at-fault accident, even if you were not the one driving the car.

It is legal to drive a borrowed car even without your own insurance. This is because car insurance follows the car, not the driver.

No. Your rates will not go up if someone gets a ticket while driving your car. This is because traffic violations are linked to a driver’s license rather than the car’s registration.

If you borrow the same car frequently, it’s a good idea to get added to the owner’s insurance policy. If this isn’t possible, buy a non-owner insurance policy.

Citations

Does Car Insurance Cover the Car or the Driver? Car and Driver. (2022).

https://www.caranddriver.com/car-insurance/a31269297/does-car-insurance-cover-the-car-or-the-driver/

Related Articles

Adding a Teen Driver to Car Insurance

June 20, 2025

What is Non-owner Car Insurance?

April 6, 2024

Short-Term Car Insurance in Arizona

April 14, 2026