Collateral Protection Insurance for Cars

Collateral protection insurance (CPI) is lender-placed coverage that protects the lender—not you—when your required auto insurance lapses, often at a much higher cost.

Get quotes from providers in your area

Last updated: June 3, 2026

Key Takeaways: Collateral Protection Insurance for Cars

Collateral protection insurance (CPI) is lender-placed coverage that protects the lender — not you — when your required auto insurance lapses.

CPI is added to your auto loan when you fail to maintain required coverage, including collision, comprehensive, and gap insurance.

CPI costs $2,400–$6,000/year — significantly more than the $2,356 national average for full coverage.

CPI does not cover your liability or medical bills; it only protects the lender’s financial interest.

To avoid CPI, keep your required coverage active and send proof of insurance to your lender.

Find out if you're overpaying for auto insurance.

See how much you could be saving! Let's get started by entering your ZIP Code:

What Is Collateral Protection Insurance (CPI)?

Collateral protection insurance, also known as CPI insurance, is a type of force-placed insurance that a lender adds to your auto loan if your personal car insurance lapses. It protects the lender’s financial interest in the vehicle—not yours—and typically offers limited or no coverage for you as the borrower.

Auto loans come with insurance requirements that are typically more than your state’s required coverage. Usually, this includes collision, comprehensive, and gap coverage, which will pay for the remainder of your loan if your vehicle is totaled. If you don’t have the insurance your auto loan lender mandates, the lender will add collateral protection insurance to your loan.

CPI insurance usually costs more than standard coverage and is added to your loan balance, increasing your monthly payments. Unlike personal auto insurance, CPI doesn’t cover your liability or medical bills.

To avoid being charged for CPI insurance, always keep your required auto insurance active and provide proof to your lender. If CPI is added in error, you can request a refund by showing valid proof of continuous coverage.

| Category | Collateral Protection Insurance | Standard Car Insurance |

|---|---|---|

| Who Buys It | The auto loan lender (and charges the cost to the borrower) | The borrower |

| Who Is Protected | The auto loan lender | The borrower (and others involved in the accident, depending on coverage) |

| When It Is Applied | When the borrower fails to maintain required car insurance | Anytime the insured vehicle is involved in a covered incident |

| What It Covers | Physical damage to the financed car, including damage from collisions, theft, vandalism, and natural disasters; does not include liability | Liability insurance (as required by the state of residence), and any additional chosen coverages |

| Annual Average Cost | $2,400 to $6,000, depending your state, lender, and driving history | $2,356 for full coverage

$722 for minimum coverage |

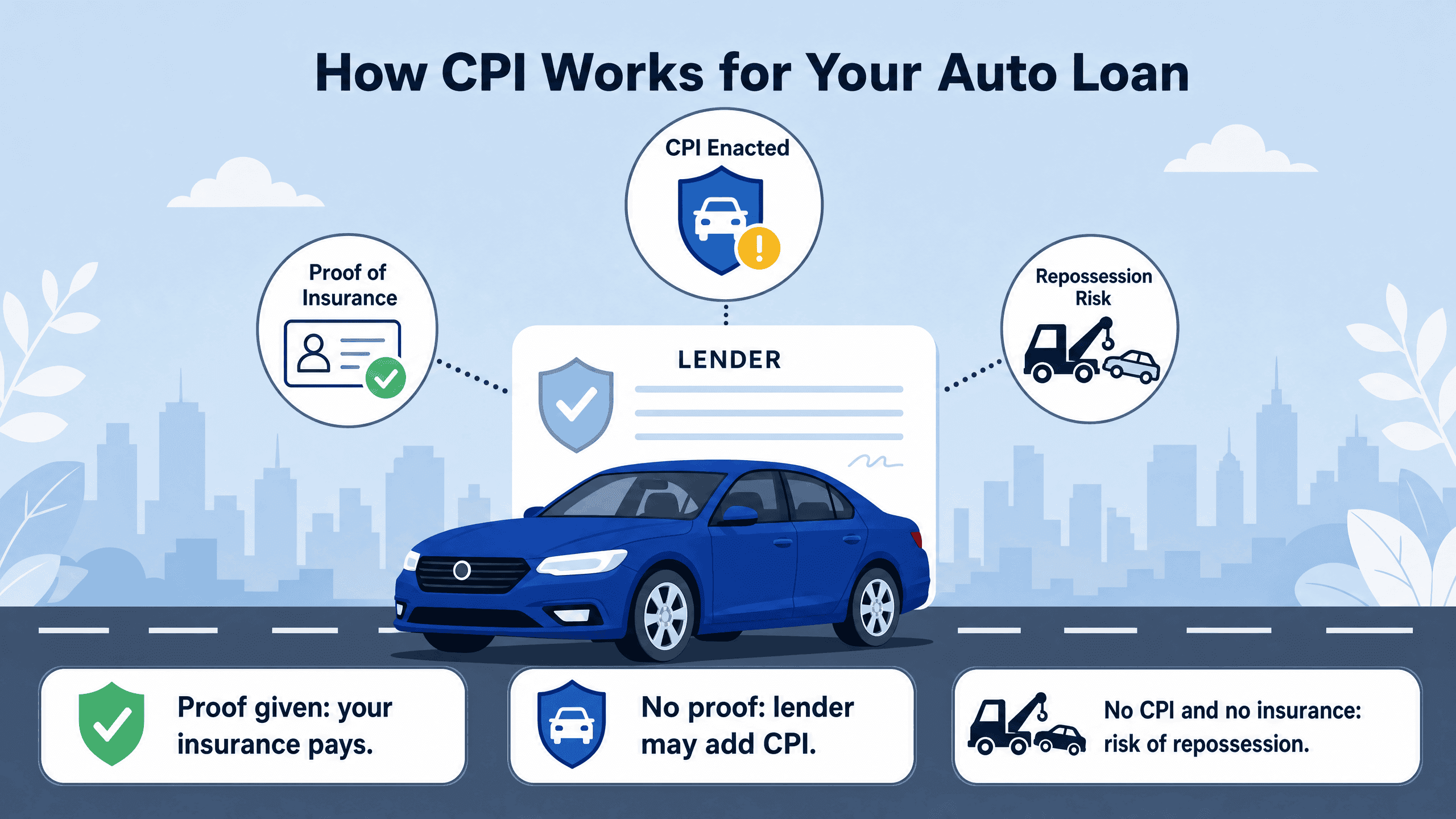

How CPI Works

Failing to provide proof of insurance to your lender can lead to collateral protection insurance or vehicle repossession.

When It’s Enacted

Typically, CPI is enacted when a borrower fails to provide proof of auto insurance coverage, including collision and comprehensive coverage and gap insurance. These coverages pay for the borrower’s property damages, whether from collisions or weather conditions, theft, vandalism, etc.

If the borrower doesn’t have collision or comprehensive coverage and their car is totaled, they may still owe an amount on their loan, which gap insurance would cover. If they don’t have gap insurance, the lender would enact CPI to recoup the loaned amount.

How It Impacts You

If you purchase the minimum coverage your lender requires, CPI won’t affect you at all. However, if you fail to provide proof of insurance, your lender may enact CPI. This means you’ll be responsible for the cost of any property damages, not your loan provider.

What Happens if CPI Isn’t in Place

If CPI isn’t in place, it means you provided the necessary proof of insurance via your insurance ID or policy declarations page. Then, if you total your car, your gap insurance will cover the remaining balance on the loan. This means the lender won’t need to protect itself with CPI.

If CPI hasn’t been enacted and you still owe money on your loan and have no insurance, your lender may repossess your car. The repossession will show up on your credit report and lower your credit score, increasing your car insurance premiums and auto loan interest rates.

NOTE:

Having a bad credit score affects your car insurance premiums in every state except California, Massachusetts, Hawaii, and Michigan.

How to Avoid CPI

- Pay your car insurance premiums to your insurance company to maintain the coverage your lender requires.

- Send proof of insurance to your lender.

- If CPI is already in place, your lender will cancel your policy once it receives proof of insurance.

How to Get a Refund

Once you show proof of insurance, your auto loan lender will refund you for the cost of the CPI. Find out more about the costs below.

Companies That Offer CPI

- Allied Solutions

- Breckenridge Insurance Group

- CUNA Mutual Group

- ISI

- Lee and Mason Financial Services

- State National

- SWBC

- Tokyo Marine Highland1

Cost

CPI costs anywhere from $200 to $500 a month or $2,400 to $6,000 a year. That’s much more expensive than the average cost of auto insurance, meaning it’s cheaper to have the required coverage and avoid CPI altogether.

How Cost Is Determined

The cost of CPI depends on your state and lender, as well as your driver risk level. Higher-risk borrowers have higher CPI premiums.2

FYI:

You won’t get to choose the type of coverage on your CPI. Your lender will decide that for you.

Is CPI/Lender-Placed Insurance Legal?

CPI/lender-placed insurance is legal. It’s part of the auto loan agreement you signed initially.

Collateral Protection vs. Force-Placed Auto Insurance

Collateral protection and force-placed insurance are two terms for the same concept, along with creditor-placed insurance.3

Conclusion

Hopefully, you won’t have to use CPI insurance as you’ll already have the coverage your auto lender requires. Since CPI costs more than auto insurance, the best bet is to maintain the coverage required. We’ve reviewed the best cheap car insurance providers to help you satisfy requirements and prevent unnecessary expenses.

Frequently Asked Questions

Collateral protection insurance (CPI) — also called lender-placed or force-placed insurance — is coverage a lender adds to your auto loan when you fail to maintain the required auto insurance. It is designed to protect the lender’s financial interest in the vehicle, not yours as the borrower. If your personal car insurance lapses, your lender can enact CPI and add the cost to your loan balance, increasing your monthly payments.

CPI itself is not something you choose — it’s automatically applied by your lender if you fail to meet their insurance requirements. Auto loans typically require more than your state’s minimum coverage, usually including collision, comprehensive, and gap insurance. As long as you maintain those required coverages and provide your lender with proof, CPI will never be applied to your loan.

CPI typically costs $200–$500 per month, or $2,400–$6,000 per year — significantly more than the national average of $2,356 for a full coverage policy. The exact cost depends on your state, your lender, and your driver risk level, with higher-risk borrowers paying more. This makes maintaining your own required coverage the far more affordable option.

CPI covers physical damage to the financed vehicle, including damage from collisions, theft, vandalism, and natural disasters. However, it does not cover your liability or medical bills — it only protects the lender’s financial stake in the car. For personal coverage, you need your own separate auto insurance policy.

The key difference is who is protected: regular car insurance protects you and others involved in an accident, while CPI protects only the lender. Standard auto insurance is purchased by you, covers liability as required by your state, and can include additional coverages of your choosing. CPI is placed by the lender without your input, covers only physical damage to the vehicle, and typically costs far more than comparable personal coverage.

Yes — the best way to avoid CPI is to keep your required auto insurance active and send proof of coverage to your lender. If CPI was added because your coverage lapsed, your lender will cancel it once you provide valid proof of insurance. You can also request a refund for any period during which you maintained your own coverage at the same time CPI was in effect.

Sources

Best Collateral Protection Insurance & Vendor Single Interest (CPI/VSI) Providers (2023) Green Profit Solutions, Inc. (2023, Jan 3).

https://greenprofitsolutions.com/blog/best-collateral-protection-insurance-cpi-providers-2019/What is Collateral Protection Insurance? Capital One. (2022, May 20).

https://www.capitalone.com/cars/learn/managing-your-money-wisely/what-is-collateral-protection-insurance/1515Property & Casualty Market Conduct Annual Statement. National Association of Insurance Commisssioners. (2021).

https://content.naic.org/sites/default/files/inline-files/MCAS-Data-Call-Lender-Placed-Home-and-Auto-v.-2021.1.0.pdf

Related Articles

What Happens if I Don’t Pay My Car Insurance?

November 4, 2025

How to Refinance a Car Loan: A Step-by-Step Guide

July 15, 2026

What happens if my car insurance policy lapses?

August 5, 2026