Last updated: April 6, 2026

Do Cars With Self-Driving Features Cost Less to Insure?

Less to Insure? Autonomous technology doesn’t decrease car insurance premiums; sometimes vehicles with these features cost more to insure, due to high repair costs.

Get quotes from providers in your area

In the past two decades, the automotive industry has made major strides in technology. In particular, electric vehicles with autonomous driving features are becoming increasingly available to the public. Electric vehicles offer reduced carbon footprints and lower fuel costs, while Advanced Driver Assistance Systems (ADAS) reduce accident rates.

Vehicles equipped with crash-prevention technology should mean lower premiums, but that’s not necessarily the case. While accidents may become less frequent, the cost to repair these high-tech machines is high.

In this guide, we’ll break down the impact of self-driving features on your rates, and what owners of major EV brands can expect when purchasing coverage.

Understanding Autonomous Driving Levels

For vehicles, there are six levels of driving automation, ranging from 0 (no automation) to 5 (full vehicle autonomy).

Right now, there is no fully automated vehicle available to the public. Most advanced systems operate at level 2, including Tesla’s Full Self-Driving system, GM’s Super Cruise, Hyundai’s Highway Driving Assist 2, and Ford’s BlueCruise. These cars can control steering and acceleration, but the driver still needs to monitor the driving.

Adaptive cruise control — which became widely standard between 2017 and 2020 — operates at level one of automation.

TIP

Never assume “autopilot” or “self-driving” marketing terms mean you can take your eyes off the road or that insurance liability shifts to the carmaker.

Right now, widely available autonomous features do not decrease car insurance premiums. Since the human is responsible, providers still calculate premiums using the driver’s history and demographics. Until we reach fully automated driving, insurance premiums will reflect the driver’s risk profile instead of the vehicle’s self-driving capabilities.

Safer Cars With Higher Premiums

According to the Highway Loss Data Institute, Advanced Driver Assistance Systems (ADAS) features reduce the frequency of claims1. For example, rear automatic emergency braking systems have lowered property damage claim rates by almost 30 percent.

However, when an accident does occur, the cost of the claim is much higher. Here’s why cars with automated features have higher car insurance rates:

- Sensor vulnerability: Sensors and cameras are often located in bumpers, fenders, and side mirrors—which are usually damaged in minor fender benders. What used to be a $500 plastic bumper repair can now be a $3,000 repair involving camera replacement and calibration.

- Calibration costs: Even after replacing a part, technicians need to calibrate sensors to communicate correctly with the car’s computer. This requires expensive software and hours of high-rate labor.

- Windshield complexity: Many ADAS cameras look through the windshield, which can triple the cost of repairs. If a rock cracks your glass, you’ll need glass from the original equipment manufacturer and a camera recalibration.

Insurance rates are based on the cost of claims, so the expense of repairing high-tech vehicles outweigh the amount saved by avoiding minor accidents.

RELATED

Check out a breakdown of the cost of owning an EV.

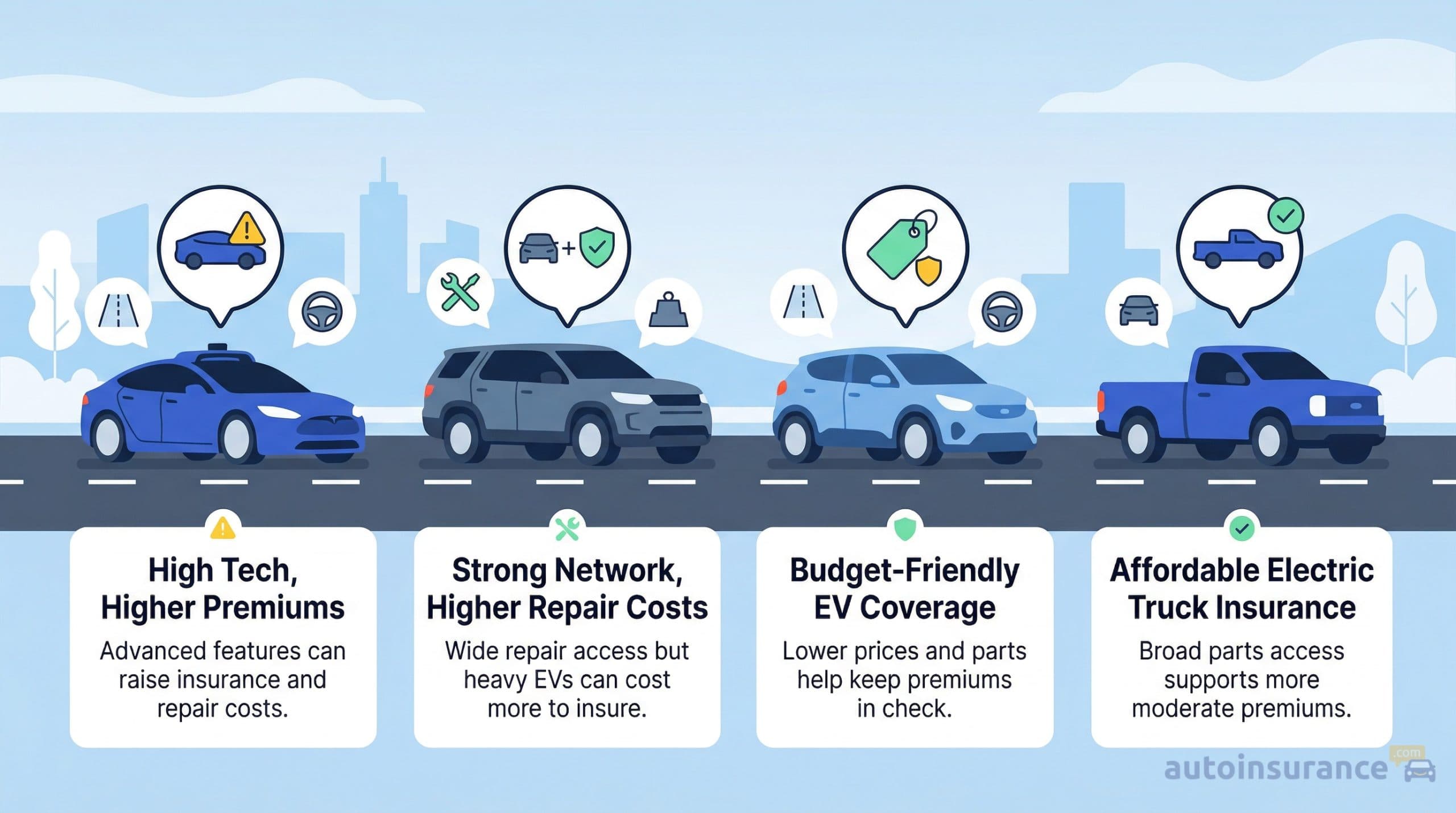

Manufacturer Breakdown: Tesla, GM, Hyundai, and Ford

If you’re planning to purchase or lease an EV, it’s important to know that the car brand will determine your car insurance rate. There are key differences between major manufacturers, like the autonomous features offered and the repair experience. Here’s how Tesla, GM, Hyundai, and Ford compare.

Tesla

While Tesla’s Full Self-Driving system has more high-tech features compared to competitors, its vehicles are expensive to insure. Tesla owners can expect high repair prices, since Tesla limits the availability of parts and restricts who can make repairs.

The company launched Tesla Insurance to make policies more affordable, using telematics data to help calculate rates. However, there are a couple things to keep in mind:

- States like California effectively bar insurers from using telematics to calculate premiums, so savings may not be as high

- City driving, which involves frequent stops and starts and proximity to other cars, will often lower a telematics score, which can cut into savings

Consider these factors when deciding whether to purchase a usage-based insurance policy.

FYI

As of January 2026, Tesla has discontinued its Autopilot system in North America. Its Full-Self Driving system is available by subscription2.

General Motors

General Motors (GM) offers Super Cruise on vehicles like the Chevy Bolt EUV, Cadillac Lyriq, and GMC Hummer EV. Super Cruise allows for hands-free driving on compatible highways.

Unlike Tesla, GM has a wide network of dealerships and body shops. If you need your GM vehicle repaired, you can find more GM-certified shops and get the parts you need. On the other hand, the sheer weight of vehicles (like the Hummer EV) and steep price of batteries lead to higher-than-average premiums.

The Chevy Bolt tends to be cheaper to insure, due to its modest purchase price and lower repair costs—but premiums will still likely be higher than for a comparable gas-powered hatchback.

Hyundai

Hyundai has positioned itself as a value-oriented EV manufacturer, with models like the Kona Electric and Ioniq 5 offering strong range and advanced features at a lower price point than many competitors. Its Highway Driving Assist system provides lane-centering and adaptive cruise control, though it is generally less advanced than Tesla’s Full Self-Driving or GM’s Super Cruise.

From an insurance standpoint, Hyundai EVs are often more affordable to insure than Tesla or luxury EVs. Lower purchase prices and more accessible parts help keep repair costs down. Additionally, Hyundai benefits from a broad dealership and repair network, making it easier to find certified technicians and replacement components.

However, EV-specific repairs—particularly battery-related issues—can still be costly, and newer models like the Ioniq 5 may carry higher premiums than older Hyundai EVs due to their technology and value.

Ford

Ford also enables hands-free highway driving with BlueCruise, which is available on the Mustang Mach-E and F-150 Lightning. Notably, the Ford F-150 Lighting boasts one of the cheapest car insurance rates for electric pickups. Ford EVs are moderately expensive to insure because owners have access to aftermarket parts and a wider repair network.

Manufacturer Comparison

| Manufacturer | Key Autonomy Feature | Insurance Cost Factor | Repair Network Accessibility

|

|---|---|---|---|

| Tesla | Self-driving | High | Low |

| GM | Hands-free highway driving | Medium-High | High |

| Hyundai | Driver assistance (Highway Driving Assist) | Medium | High |

| Ford | Hands-free highway driving | Medium-High | High |

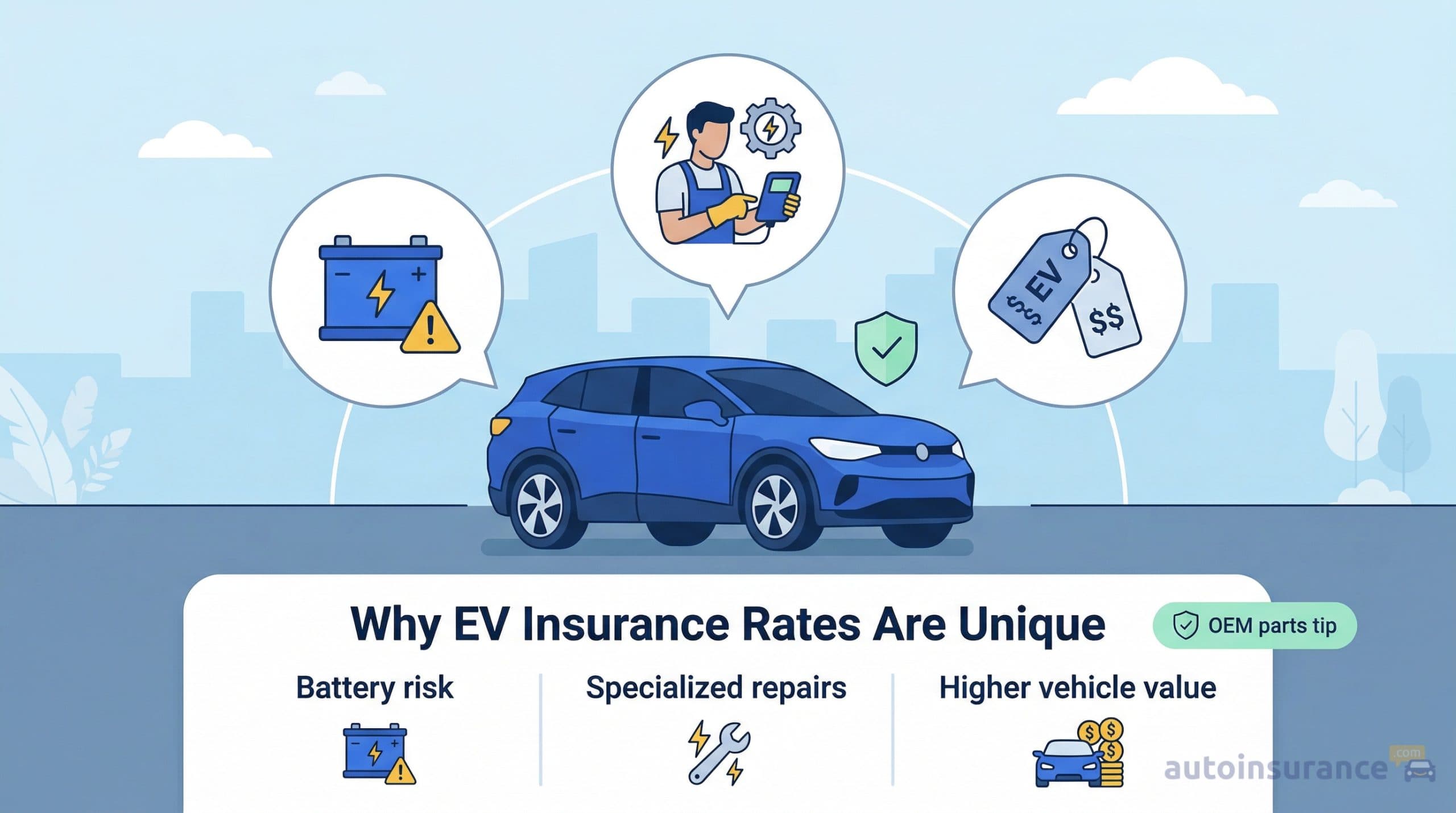

Why EV Insurance Rates are Unique

Owning an electric vehicle means facing specific circumstances that drive the cost of car insurance rates. Here are three factors that make an EV more expensive to insure:

High-Voltage Battery Replacement

The battery is the most expensive part in an electric vehicle, costing between $10,000 and $20,000. If the battery casing is damaged in a crash, providers usually require a total replacement because of fire risk. As a result, a moderate accident with an EV can result in a total loss, leading providers to charge higher premiums to cover their risk.

Specialized Labor Shortages

While more drivers adopt electric vehicles, the number of qualified mechanics trails behind. Independent repair shops face high costs and risks to repair EVs, including training technicians and facing electrocution risks.3

Labor time (except painting) for EVs is double the average for non-EVs, and paint labor time is 50 percent higher4. The higher labor time and costs translate to higher premiums.

Higher Market Value

EVs have a higher purchase price than gas-powered cars, which drive up car insurance rates. If you own a $55,000 Mustang Mach-E, it will cost more to insure than a $30,000 Ford Escape because the payout in a total loss incident is higher.

TIP

Check if your insurer offers original equipment manufacturer coverage. Using aftermarket parts on high-tech EVs can sometimes void manufacturer warranties.

Will Electric Vehicle Premiums Drop?

While EV insurance rates are high, there are several factors that may lower the cost of insuring electric vehicles with autonomous features. Over time, these rates may dip below premiums for gas-fueled vehicles.

Standardization of Technology

As blind-spot monitoring, automatic braking, and lane-keeping assist become standard features, the cost of the sensors will decrease. Repair shops will also become more proficient at calibrating them, reducing labor times.

Shift in Liability Laws

Eventually, as we move toward fully autonomous vehicles, liability may shift from the driver to the manufacturer. If the car is driving itself, the manufacturer (or the software provider) assumes the risk. This could transform the auto insurance industry, transferring the costs from vehicle owners to the automaker through product liability policies.

Data-Driven Pricing

Telematics will have a bigger role in determining rates, and providers will rely on fewer factors like credit score. Autonomous vehicles that prove they are driving safely could receive substantial discounts, rewarding owners for investing in safety tech.

How to Lower Your EV Insurance

Here’s how to find the best EV insurance and pay less for your policy:

- Compare providers: Look into tech-forward carriers like Lemonade or Root, which can use telematics to offer fairer pricing.

- Bundle policies: This remains one of the most effective ways to save. Bundling your EV auto policy with home or renters insurance can save you up to 25 percent.

- Utilize green discounts: Some car insurance companies have specific discounts for hybrid and electric vehicles. Ask if providers offer a green vehicle discount.

- Shop before buying: Before signing the papers for a new Rivian or Ford Lightning, get the VIN and run insurance quotes. It’s better to be prepared so you don’t spend more than expected on insurance.

Frequently Asked Questions

No — while self-driving features reduce the chance of an accident, they’re more likely to raise premiums due to the high cost of repairing the system’s complex sensors. Most insurers still determine rates based on your driving profile, instead of the software’s capability.

EVs are typically more expensive to insure than gas-powered cars. They have higher repair costs, specialized labor requirements, and higher market values.

Tesla Insurance may offer lower premiums for drivers who live outside of urban areas, where driving patterns can lower the telematics discount. However, for drivers in cities or with aggressive habits, rates can be higher than standard policies.

Lower-value EVs with widely available parts, like the Nissan Leaf or older Chevrolet Bolt models, are the cheapest to insure. They lack the performance and complex luxury features of high-end models.

Yes, comprehensive and collision policies cover battery damage resulting from an accident or covered peril. However, car insurance policies don’t typically cover normal wear and tear or battery degradation, as they’re considered maintenance costs.

No, a standard auto policy covers these vehicles, as long as you hold comprehensive and collision coverage.

Conclusion

While the safety benefits of autonomous features are undeniable, it’s not yet reflected in car insurance costs. Owning a high-tech vehicle means paying higher premiums to enjoy cutting-edge performance and safety.

However, the long-term looks more promising. As specialized parts become standard and autonomous technology verifies its safety record over billions of miles, we expect premiums to decrease. Until then, being proactive can help you find affordable premiums for your EV.

Citations

Compendium of HLDI Collision Avoidance Research. Highway Loss Data Institute (HLDI). (2023, April).

https://www.iihs.org/media/d391f0fa-2c92-4308-a27f-c93d60757e55/3VeIsw/HLDI%20Research/Collisions%20avoidance%20features/40-04-compendium.pdf

Tesla Discontinues Autopilot, Shifts FSD to Subscription-Only. Auto Body News. (2026, January 23).

https://www.autobodynews.com/news/tesla-discontinues-autopilot-shifts-fsd-to-subscription-only

EV Broken? Finding a Technician to Fix It May Take a While. Reuters. (2023, September 6).

https://www.reuters.com/business/autos-transportation/ev-broken-finding-technician-fix-it-may-take-while-2023-09-06/

Will Electric Vehicle Regulations Continue to Force Change?. CCC Intelligent Solutions (CCCIS). (2023, July 11).

https://www.cccis.com/news-and-insights/posts/will-electric-vehicle-regulations-continue-to-force-change

Related Articles

Most EV-friendly cities in the U.S.

April 2, 2026Farm Bureau Car Insurance Review 2026

March 31, 2026