Can You Get Full Coverage Insurance Under $50 a Month?

Getting full coverage car insurance for less than $50 monthly is unlikely, but there are steps you can take to keep your rates as low as possible.

Get quotes from providers in your area

Last updated: June 5, 2026

Key Takeaways

- On average, full coverage auto insurance costs $196 per month, or $2,356 per year.

- The cheapest full coverage options fall between $130 and $160 monthly, depending on where you live and assuming a clean driving record.

- If you don’t drive often, you can get cheaper auto insurance rates with a pay-per-mile policy — potentially around $110 monthly.

- Those seeking the absolute lowest auto insurance rates should consider minimum coverage instead of full coverage.

Find out if you're overpaying for auto insurance.

See how much you could be saving! Let's get started by entering your ZIP Code:

Can You Get Full Coverage for Less Than $50 a Month?

It’s extremely rare to find full coverage car insurance for under $50 a month. While rates vary based on your location, age, driving history, credit, and vehicle type, the national average for full coverage is about $196 per month ($2,356 annually). That’s almost four times the $50 mark.

Minimum coverage is typically much cheaper. The average cost of minimum coverage in the U.S. is around $60 per month, with some insurers offering policies as low as $36 per month or less. However, these plans don’t offer the same level of protection as full coverage. Additionally, if you financed or leased your car, your lender likely requires you to carry full coverage.

Cheapest Full Coverage Auto Insurance Providers

For a traditional unlimited mileage policy, USAA, Travelers, and GEICO are major providers that offer some of the cheapest full coverage rates. Regional providers Plymouth Rock, Auto-Owners, and Erie also offer cheap rates, as does Connect, which is available to Costco members.

The table below shows the cheapest full coverage auto insurance providers in the country.

| Provider | Monthly full coverage | Annual full coverage |

|---|---|---|

| USAA | $128 | $1,533 |

| Plymouth Rock | $138 | $1,656 |

| Connect (Costco) | $138 | $1,660 |

| Erie | $153 | $1,833 |

| Travelers | $153 | $1,837 |

| GEICO | $156 | $1,867 |

| Auto-Owners | $156 | $1,870 |

| Nationwide | $166 | $1,987 |

| Clearcover | $169 | $2,023 |

| State Farm | $169 | $2,030 |

| Progressive | $172 | $2,060 |

Cheapest Pay-Per-Mile Insurance

Pay-per-mile insurance can provide significant savings for low-mileage drivers such as remote workers.

If you drive infrequently, you may be able to pay less for full coverage car insurance with a pay-per-mile policy. With this type of policy, you pay a set monthly or daily base rate, plus a per-mile rate. How much you pay per month varies depending on how much you drive.

Here’s an example based on advertised rates from Nationwide Smartmiles:

| Base rate | $54 monthly |

|---|---|

| Per mile rate | $0.06 per mile |

| Monthly rate, assuming 500 miles driven | $84 (= $54 base rate + $30 mileage rate) |

It’s worth considering a pay-per-mile policy if you drive fewer than 7,500 miles annually. People who may drive less than average include:

- Remote workers

- Retirees

- Stay-at-home parents

- Households with an extra car

Nationwide SmartMiles offers some of the cheapest pay-per-mile insurance, with an average annual rate of $1,697 and an average monthly rate of $141. For military-affiliated drivers, USAA also offers low-cost pay-per-mile insurance, with an average annual cost of $1,282 and an average monthly cost of $107.

Note that cost varies widely depending on how much you drive and where you live. Additionally, data is not available for all pay-per-mile providers. Compare quotes from at least three providers to find the cheapest rates for you.

| Provider | Annual full coverage average | Monthly full coverage average |

|---|---|---|

| USAA SafePilot Miles | $1,282 | $107 |

| Nationwide SmartMiles | $1,697 | $141 |

| Root | $1,719 | $143 |

| Allstate Milewise | $2,447 | $204 |

| Mile Auto | Data not available | Data not available |

How to Save on Full Coverage

While the national monthly average cost of auto insurance is $196 a month, there are steps you can take to keep your monthly rates as low as possible:

Shop Around for Discounts

Many providers offer a wide range of auto insurance discounts, including safe-driver discounts, low-mileage discounts, and even alumni or teacher discounts. Not all insurers have the same discount offerings, so shop around for ones that apply to you.

FYI:

Low-mileage discounts differ from pay-per-mile insurance. Pay-per-mile insurance bases your rate on the number of miles you drive, whereas a low-mileage discount gives a percentage discount on your standard auto insurance rate if you don’t exceed a certain number of miles.

Increase your Deductibles

Higher deductibles typically mean lower monthly premiums. Generally, a $1,000 deductible strikes a good balance, but if you’re trying to maximize savings, you might opt for a $1,500 or $2,000 deductible. Remember, the higher your deductibles are, the more you’ll need to pay out of pocket if you get into an accident. Before you take this step, make sure you can afford the out-of-pocket costs.

Trim Nonessential Coverages

Instead of opting for a complete full coverage policy, consider removing any nonessential coverage types, like roadside assistance and rental car reimbursement.

Practice Safe Driving Habits

A DUI, speeding ticket or accident on your record can significantly increase the cost of your auto insurance. Always practice safe driving habits to keep your rates as low as possible. Insurance companies typically look back three to five years on your record when determining your rates, so if you do have a violation, your rates should decrease as time passes.

Improve your Credit Score

A low credit rating can increase your auto insurance rates significantly — sometimes by even more than a DUI. If you improve your credit score, you’ll likely see your rates decrease along with it.

Choose a Practical Vehicle

Lower-value vehicles are typically cheaper to insure than luxury vehicles. In addition, some companies offer discounts for safety features such as anti-theft devices, airbags, or passive restraint devices.

Compare Quotes

We recommend comparing quotes from at least three companies to find the lowest car insurance rates possible.

Cheapest and Most Expensive States for Full Coverage Auto Insurance

One of the most significant factors in your auto insurance rates is your location. Below, we’ll review some of the cheapest and most expensive states for full coverage auto insurance.

Cheapest States for Full Coverage Auto Insurance

On average, Vermont has the lowest average full coverage car insurance rates at $1,478 per year, or $123 per month. Maine and Idaho have the next-cheapest average rates, with full coverage at $127 and $129 per month, respectively.

| State | Annual full coverage | Monthly full coverage |

|---|---|---|

| Vermont | $1,478 | $123 |

| Maine | $1,526 | $127 |

| Idaho | $1,549 | $129 |

| New Hampshire | $1,602 | $134 |

| Wyoming | $1,616 | $135 |

Most Expensive States for Full Coverage Auto Insurance

On the other end of the scale, Florida has the highest average rate for full coverage auto insurance at $3,672 per year, or $306 per month. Louisiana ($304 per month), Nevada ($281 per month) and Michigan ($251 per month) have the next-highest monthly rates.

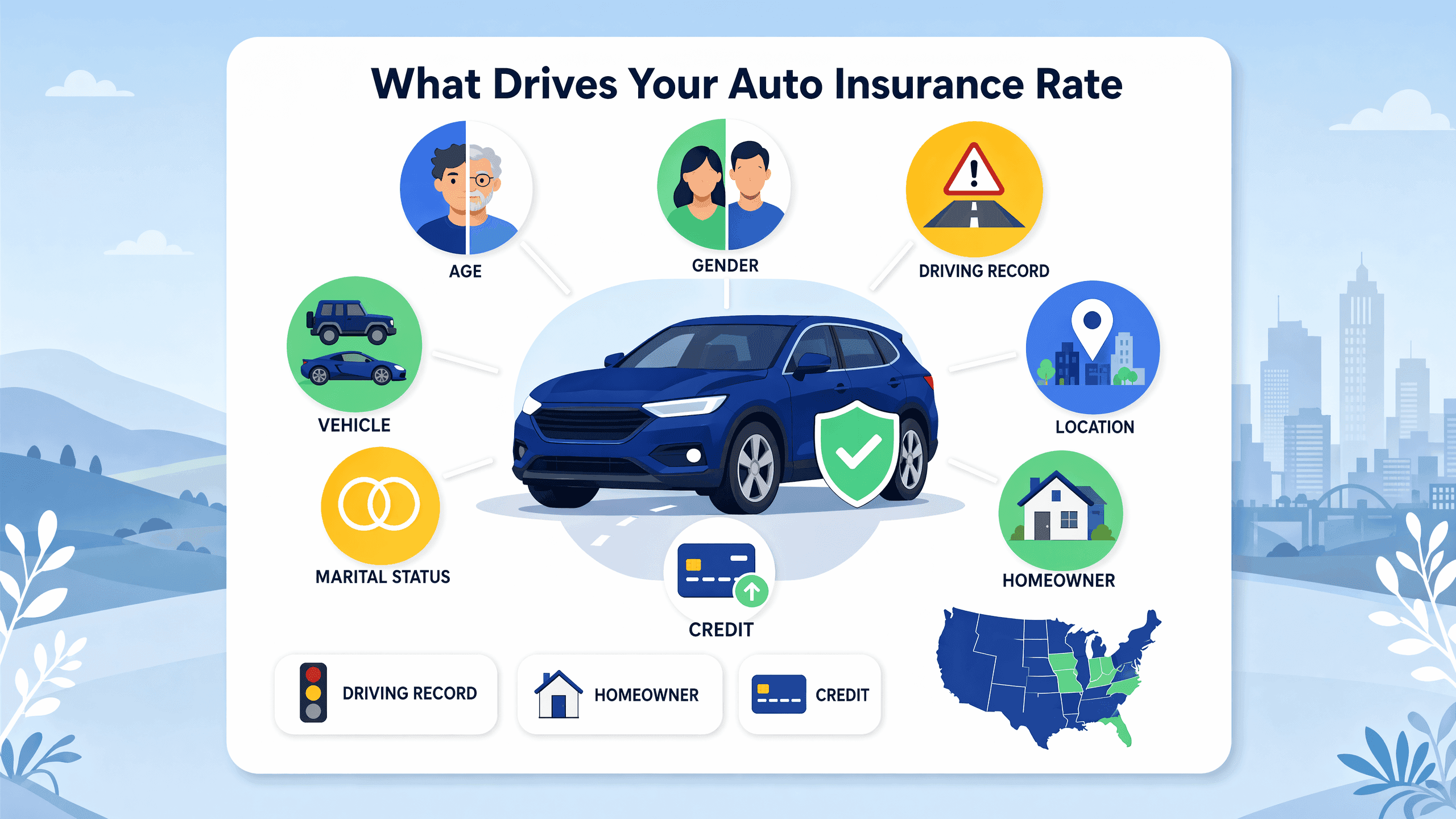

Factors That Influence Your Auto Insurance Rates

Your auto insurance premium is influenced by personal demographics, driving history, and location.

Regardless of which coverage type you choose, multiple factors affect your auto insurance rate, including your age, location and marital status.

- Age: Car insurance is often the most expensive for young drivers and the cheapest for those in their 30s and 40s, and rates tend to increase again as drivers get older.

- Gender: Many providers charge higher rates for men than for women because they view men as a higher risk; the gap is widest for teenage and young adult drivers.

- Driving history: Your driving history has a significant impact on your auto insurance rates. A history of DUIs, speeding tickets or at-fault accidents can raise your rates by 20 to 94 percent.

- Vehicle: Some vehicles cost more to insure than others. Luxury and sports vehicles cost more; SUVs and sedans typically cost less.

- Location: Your state and city have a big influence on your insurance rates. Drivers in dense, urban areas experience higher costs.

- Marital and homeowner status: Drivers who are married or own their own home often get lower insurance rates.

- Credit score: On average, a low credit score will increase your auto insurance by 72 percent, almost as much as having a DUI on your record.

DID YOU KNOW?

Massachusetts, California, Hawaii and Michigan are the only states that do not consider your credit score when determining your auto insurance rates.

Full Coverage vs. Liability: Which Is Best?

Whether full coverage or liability coverage is best for you depends on your personal risk tolerance and monthly budget. For many drivers, the higher cost of full coverage is well worth the additional peace of mind that vehicle and medical costs will be covered in the event of an accident.

When You Should Get Full Coverage

If you fall into any of the below categories, full coverage is a good idea:

- Have a brand-new car

- Cannot cover the costs of an accident out of pocket

- Live in a high-risk neighborhood (either due to vandalism, dangerous driving or extreme weather)

- Lease or finance your car (your lender will likely require full coverage)

When You Should Get Liability Coverage

On the other hand, liability coverage may be best if you drive an older vehicle that is fully paid off. As a rule of thumb, if annual comprehensive and collision premiums are greater than 10 percent of the car’s value, it may not be worth it.

Remember, while opting for liability coverage may save you money in the short term, you’ll likely incur much higher out-of-pocket costs if you ever need to make a claim.

TIP:

If you do opt for minimum coverage, it’s still wise to raise your limits above the required legal limits — experts recommend at least 100/300/100 — for additional protection.

Conclusion

In recent years, auto insurance rates have increased significantly1, making it highly unlikely (but not impossible) to find full coverage for less than $50 a month. If you drive infrequently, getting a pay-per-mile policy can potentially get your full coverage rates under $110 monthly.

Taking steps like researching discounts, comparing multiple providers, and determining which provider offers the lowest rate in your state, you can keep your rates as low as possible. Maintaining a clean driving record is also one of the most effective ways to keep your auto insurance rates low. If you’re seeking the absolute lowest monthly rates, consider liability coverage instead of full coverage.

Frequently Asked Questions

Among major providers, USAA ($128 monthly), Connect by COSTCO ($138 monthly), Travelers ($153 monthly), and GEICO ($156) have the cheapest average car insurance rates. Regional providers like Plymouth Rock ($138 monthly), Erie ($153 monthly), and Auto-Owners ($156 monthly) also have cheaper rates.

If you drive infrequently, you may find the cheapest car insurance with a pay-per-mile provider like USAA SafePilot Miles ($107 monthly) or Nationwide SmartMiles ($141 monthly).

In some instances, you may be able to find auto insurance for less than $50 a month, but you’ll likely need to choose minimum coverage or remove some coverages from your full coverage policy. Auto insurance rates vary significantly depending on many factors, such as your age, vehicle, driving history, credit score and location.

USAA has the lowest auto insurance rates in the country, at just $36 a month for minimum coverage. On average, minimum coverage costs $60 per month, with some providers offering lower rates. At just $128 per month, USAA has the lowest full coverage rate. For non-military drivers, regional provider Plymouth Rock has the cheapest rates, at $138 per month.

To find the lowest rates possible, look for discounts, maintain a clean driving record, and get multiple quotes.

If your annual collision and comprehensive premiums are less than 10 percent of your car’s value, full coverage is usually worth it. For example, if your annual collision and comprehensive premiums are $1,800, and your car is worth $18,000 or more, it’s worth having full coverage. Full coverage auto insurance can provide valuable peace of mind because it means receiving greater financial protection if you’re in an accident. Remember, if you opt for minimum coverage, you’ll end up paying much more out of pocket if you’re in an accident.

Sources

Why Are My Insurance Premiums Increasing?. NAIC. (2024, Nov 19).

https://content.naic.org/article/why-are-my-insurance-premiums-increasing

Related Articles

Can You Get Car Insurance With a Suspended License?

October 9, 2024

Full Coverage vs. Liability Car Insurance

July 22, 2025

Can You Get Auto Insurance Without a License?

July 24, 2024